Despite facing multiple challenges such as overcapacity, low factory utilization, and geopolitical volatility, the Wafer Fabrication Equipment (WFE) market maintains a steady growth trajectory driven by technological innovation, device architecture evolution, and leadership from top-tier enterprises. It is projected that by 2030, the market size will rise to $184 billion.

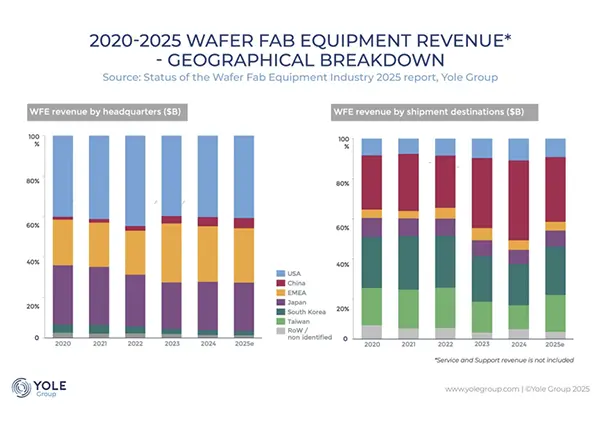

Currently, the semiconductor industry exhibits significant overcapacity and structural redundancy. While wafer foundries and Integrated Device Manufacturers (IDMs) grapple with declining utilization rates and profit pressure, investments in equipment continue unabated. Behind this paradox lies the strategic consideration of governments and enterprises worldwide, which prioritize technological sovereignty and supply chain resilience over short-term profitability.

The redundant construction of wafer fabs in multiple regions has exacerbated resource redundancy, yet it has also sustained continuous demand for WFE tools. As a result, equipment suppliers have unexpectedly benefited from the geopolitically driven market structure, rather than purely market logic.

The WFE market has long been dominated by five major suppliers: ASML, Applied Materials, Lam Research, Tokyo Electron Limited (TEL), and KLA Corporation. By 2024, they collectively held nearly 70% of the market share:

Leveraging its absolute leadership in Extreme Ultraviolet (EUV) lithography, ASML accounted for approximately 20% of the market in 2023 and 2024, firmly securing the top position in the industry.

Applied Materials maintained its advantage in deposition and materials engineering, with a market share of nearly 20% in 2022.

Lam Research and TEL each held around 10% of the market, with solid positions in key process segments such as etching and deposition.

KLA, focusing on inspection and metrology with a share of approximately 7%, is a key player in this field.

High technological barriers, capital intensity, and long-term cooperative relationships with chip manufacturers have consolidated this market structure.

Segmented Markets: Diverse Growth Paths Driven by Processes and Applications

From the perspective of equipment types, lithography equipment accounted for the largest market share (26.5%) in 2024, followed by deposition equipment, etching & cleaning equipment, and metrology & inspection equipment. Looking ahead to 2030, growth varies across segments:

Wafer bonding, though relatively small in market scale, will become the fastest-growing segment with a 10.4% compound annual growth rate (CAGR).

Etching & cleaning equipment will grow at a CAGR of 5.5%.

Ion implantation equipment will see the slowest growth, with a CAGR of only 2.0%.

In terms of application drivers, advanced logic devices of ≤7nm have become a key investment focus, with a 7% annual growth rate. Other important growth areas include:

DRAM using EUV lithography,

Logic devices above 7nm,

NAND memory with superlattice layers and multi-stack designs,

Specialized devices based on non-silicon materials,

Advanced packaging, and

Engineering wafers.

Technological innovation remains the core driver of industry development. Between 2024 and 2030, logic devices will evolve from FinFET to Gate-All-Around (GAA) and even Complementary FET (CFET) architectures; DRAM will begin to adopt EUV lithography and advance toward 4F² high-density architectures; and NAND memory will increase storage density by adding more stacking layers. These technological evolutions require equipment suppliers to provide not only hardware but also comprehensive process solutions that integrate upstream and downstream needs.

Equipment suppliers must offer modular solutions that balance specialization and flexibility to adapt to diverse process requirements.

Conclusion

The wafer fabrication equipment market profoundly reflects the contemporary paradox of the semiconductor industry: overcapacity coexists with profit pressure, and technological innovation is intertwined with geopolitical factors. Nevertheless, driven by the competition for technological sovereignty and intense rivalry among equipment manufacturers, the market will maintain a 4%-5% annual growth rate, reaching a scale of $184 billion by 2030. The enterprises that succeed in the future will be those that strike the optimal balance between specialization and flexibility, and can provide modular process solutions adapted to the continuous iteration of technology.

(Reprinted from https://news.eccn.com/)